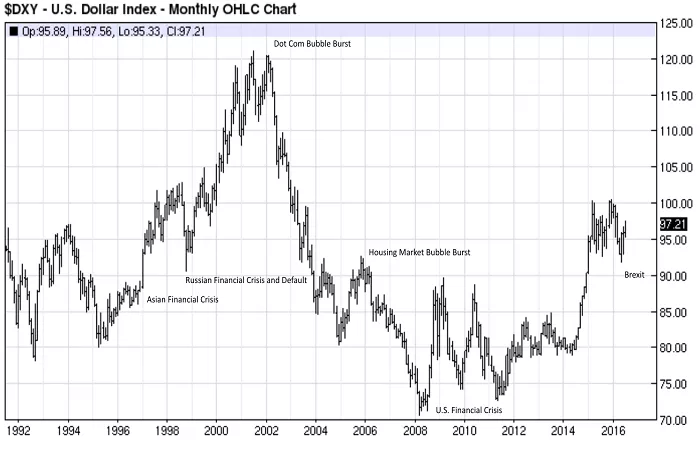

The US Dollar Index (DXY) has staged a remarkable comeback recently. As demand for American assets has skyrocketed and the prospects of a Federal Reserve interest rate cut have diminished, the index has seen a significant upswing. Tracking the dollar’s performance relative to other major currencies, the DXY climbed to $101.65, hitting its highest level since April 10. This represents a substantial 3.80% increase from the lowest point recorded this year. The question now on everyone’s mind is: does this mark the end of the USD’s downward spiral?

US Dollar Index Soars After China Trade Deal

The DXY experienced a sharp jump following the United States reaching a temporary truce with China regarding trade. On Monday, Trade Secretary Scott Bessent announced in a statement that the two countries would reduce tariffs for a three – month period to work towards a comprehensive trade agreement. The US has now decreased its tariffs on Chinese goods to 30%, while China has lowered its tariffs to around 10%. Moreover, if China shows greater commitment in combating the fentanyl crisis, US tariffs could potentially be reduced further.

This trade truce led investors to pour back into American assets such as stocks and bonds, causing the DXY to surge. US stock indices, including the Dow Jones, Nasdaq 100, and S&P 500, witnessed substantial gains, rising by 2.8%, 3.25%, and 4.35% respectively. Similarly, as demand for US bonds increased, bond yields dropped slightly. The 10 – year yield fell to 4.53%, while the 30 – year and 1 – year yields declined to 4.8% and 4.08% respectively. This is in stark contrast to what occurred when Donald Trump initiated tariffs in April. At that time, the dollar plummeted as investors anticipated a continuous decline in the demand for the greenback.

Upcoming US Inflation Data

The next significant factor that could influence the US Dollar Index is the impending release of consumer inflation data. Economists predict that the data will show a slight increase in headline consumer inflation in April. The Consumer Price Index (CPI) is expected to register at 0.3%, an uptick from the previous month’s 0.1% decrease. On an annual basis, the CPI is projected to remain at 2.4%. The core CPI, which excludes the highly volatile food and energy sectors, is anticipated to stay unchanged at 2.8% year – over – year.

There are already signs that some companies are raising prices to offset tariff – related margin pressures. For example, companies like Shein and Temu have hiked prices by more than 100% due to the expiration of the de minimis program. This program previously allowed them to ship items worth less than $800 without paying any taxes. Analysts believe that the US – China trade deal will help moderate inflation in the coming months, as companies will now only need to pay a 30% tariff. However, inflation is likely to remain considerably higher than its current level, as the US has insisted on maintaining a baseline 10% tariff. Analysts at Goldman Sachs project that US inflation will end the year at 3.8%, significantly higher than the current 2.4%. As a result, most analysts do not expect the Fed to cut interest rates in the near future.

Related topics